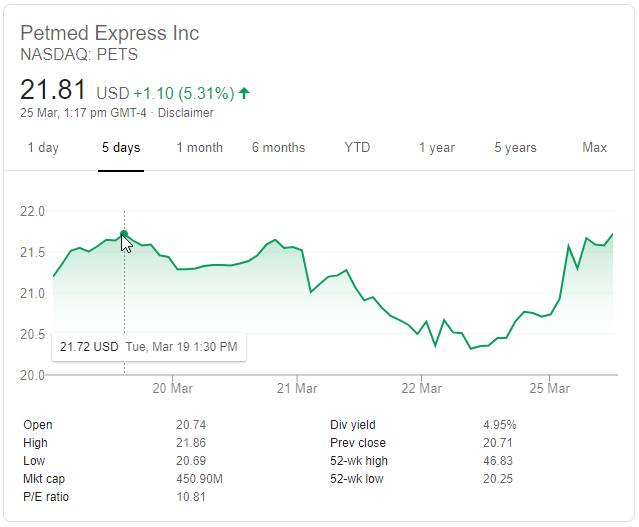

Weyerhaeuser (WY) slid hard shortly after open, so I increased the position size on it & then after turned up sold it. Petmed Express (PETS) and Funko (FNKO) were both strong today, so I sold out on those as well. A 5-day chart of PETS shows how ridiculous the stock action was.

buy the swoop, sell the eroooo

I flipped a bit of MMYT at a profit, though am still holding a mid-sized position which is down a couple hundred (though far less than I have made on that ticker so far this year or what I made on it last year). MMYT has limited trading volume, so when you couple that with an emerging market growth stock, volatility & spreads can be quite high, so you need it to move a bit to make up for the bid/ask spreads.

I am holding a bit of Newmont (NEM) still along with a tiny position in Kroger (KR) I just established today.

My CVS & Walgreens Boots Alliance (WBA) are still off a bit, both having stunk once more today. If I didn’t already have positions in them I would buy with size at current prices. Walgreens announces earnings next Tuesday. A big part of why WBA sold off was in conjunction with the bad quarter & write down CVS belched out recently. If Walgreens reports anything other than absolutely horrific quarter on Tuesday I think they’ll likely gain at least a couple percent & could see them gaining as much as 5%.

I can sit around & watch the market, but I don’t see any of the great opportunities I saw earlier today, so I am off for a nap. 🙂

It appears as though Winnie the Pooh has figured out the market.

On ultra dovish Fed the market jumped slightly & then sold off, then was on fire the following day & on day 3 just ahead of a weekend it appears to have changed directions once more.

Yesterday even some low beta value plays were up 2 or 3 percent. Today many of those have given back a percent or more.

I sold my remaining Kroger (KR) near open & they’ve since slid a bit. Yesterday I sold my remaining Weyerhaeuser (WY).

One of the stocks that didn’t take part in the rally yesterday (& in fact slid a bit) was PetMeds Express (ticker symbol PETS). They trade at about a 10X P/E ratio & are close to the 2018 December panic lows. They have no debt & about a quarter of their market cap is cash on hand & inventory, so their actual PE is closer to about 7.5 or 8. Their dividend yield is above 5% now. They actually slid a bit more today & were within pennies of new lows before jumping a bit.

The thesis for why they would be a doomed value trap with no hope would be that Chewy keeps eating marketshare (more memorable brand name, faster growth, sells a broader array of products, is playing the Amazon.com growth over profits model, etc.) as the debt-levered parent company PetSmart got a reprieve from genuine market prices on debt as the Federal Reserve hinted at the QE lite program they’ll soon engage in.

On the surface, the sharp decline in 2 year yields did not seem to make sense following the FOMC decision. After all. the Fed was dovish but did not show signs of cutting rates, but the 2-year yield went through the fed funds rate. That did not seem to make sense. However, when taking into account the QE-lite policy that will heavily skew toward the short end of the curve, the move makes more sense. Not to mention when taking into account the lack of FOMC conviction on returning to hikes, the decline in the 10-year also makes sense. … This might be one of the more underappreciated FOMC decisions in recent memory. The Fed is unequivocally retreating from any further tightening for the foreseeable future. How powerful will QE-lite prove to be? That is difficult to answer, but it is likely to show itself most forcefully in the dollar and lower short-term yields.

Samuel E. Rines, Avalon Advisors

According to S&P Global Ratings on November 8, 2018, PetSmart had the following debt structure:

$955 million asset-based revolving credit facility (ABL revolver) (ABL agreement dated as of March 11, 2015)

$4.3 billion first-lien term loan (credit agreement dated as of March 11, 2015)

$1.35 billion first-lien secured notes (indenture dated as of May 31, 2017)

$2.55 billion unsecured notes (indentures dated as of March 4, 2015, and May 31, 2017)

PetSmart’s owners thought embracing e-commerce would keep it competitive in the age of Amazon.

Two chief executives and $3 billion later, they’re discovering it takes a lot more than web smarts to outrun an avalanche of debt.

The nation’s leading pet supplier has to figure out how to pay $8.1 billion in bond and loan maturities even as its sales and margins are shrinking. Half that debt traces back to a 2015 buyout led by private equity firm BC Partners, whose bidding was so aggressive that it actually topped its own offer to seal the deal, leaving veteran rivals agog at the final price.

PetSmart’s bondholders had been expecting a spinoff of some of the equity in Chewy.com for months as the performance of PetSmart’s brick-and-mortar stores lagged behind while Chewy.com continues its rapid growth.

The company’s same-store sales have been falling for several quarters. By contrast, Chewy.com’s revenue jumped 81% to $760 million in its most recent quarter. Despite surging sales, the e-commerce business is still losing money.

That makes the justification for larding up so much debt on the company sort of moot (at least until the debt can be restructured & they force losses onto bondholders to lower the overall debt load). But seeing declining in-store sales, mounting losses on their online play, ongoing legal disputes with bondholders, etc. … Add that to the huge wave of IPOs that will come to market (Uber, Lyft, Slack, AirBNB, etc.) before Chewy.com could be fully spun out & an Amazon.com that is using ad revenues & cloud hosting profits to compete on prices … I don’t see how Chewy.com could IPO anytime soon.

Virtu was off a couple percent today but quickly recovered. Anytime the market keeps bouncing back and forth that one is frequently a solid play for a quick gain if it slides, as eventually some figure the outsized day to day churn ends up leaving more meat on the bone for an HFT market maker. Virtu sold off more in the July to October timeframe & then started improving as the broader stock market sold off.

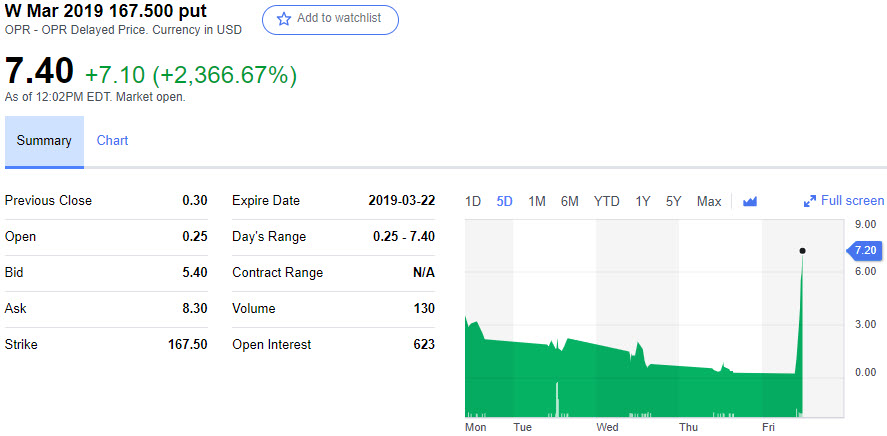

It looks like the market had a delayed reaction to the Fed’s move & that Wayfair put I bought the other day just shot the moon.

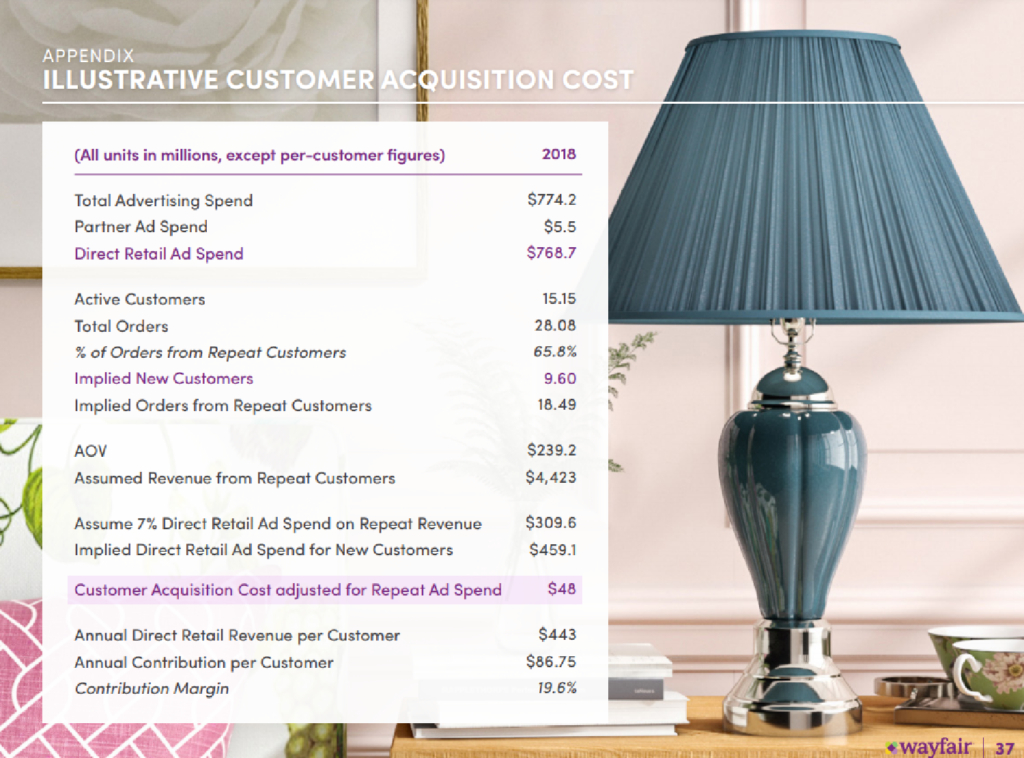

Last year, Wayfair’s operating expenses grew 8.5 percentage points faster than sales, causing operating losses to double. Despite this seeming lack of operating leverage, not all of Wayfair’s cash expenditures are accounted for on its profit and loss statement. Deep in the weeds of its 10-K, Wayfair discloses that it capitalises its “site and software development costs”, before amortising the asset over two years. In 2018, this had the effect of reducing operating losses by $63m, all else being equal. … In the face of less predictable and lumpier revenues, the market seems to think Wayfair’s future deserves the loftiest of valuations. Excluding Amazon, Wayfair’s 2.3 price-to-sales is higher than all its rivals, including The Home Depot, RH and Bed, Bath and Beyond, according to S&P Capital IQ. Of this bunch, it also has the second lowest gross margin — just 23.4 per cent — behind pseudo-crypto company Overstock.

Options are so much harder to trade than stocks because their value decays so fast unless the trade works out quickly. Wayfair aggressively promotes their growth narrative while their CEO sells ~ $5 million in stock each week & the shorts have been getting killed for years on it.

assumed, adjusted, etc.

Great comment on the FT on their above linked article about Wayfair

Demand is highly cylical and intimately tied to housing sales.

Supply is often highly geared (e.g. DFS ‘buy’ now and don’t pay for a year) and dependent on credit sales (4 year or more) with a consequent high risk of default. Unlike cars, second-hand repossessed sofas have minimal value.

People buy furniture when they move house, and if and when it falls apart. It’s surprising how long you can make a sofa last, and tables can last forever. … Nearly all the furniture retail companies I have profiled over the years have gone bust, no matter how big.

Coming into today lots of people were net long ahead of the Federal Reserve announcement & remembered the pain of the prior two meetings, so there was a sell off early in trading.

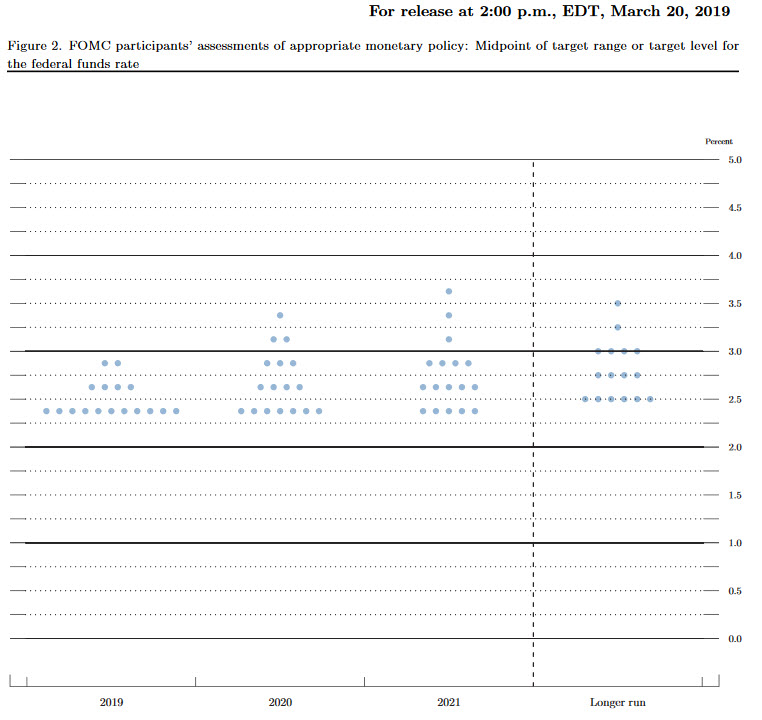

Those who put money to work ahead of the Fed’s announcement saw decent gains as the market recovered somewhat on the new scatter plots showing a low likelihood of any hikes this year & perhaps only about1 to at most 2 more hikes until rates are fully normalized over the longer term along while stating policy is currently neutral.

The Committee intends to slow the reduction of its holdings of Treasury securities by reducing the cap on monthly redemptions from the current level of $30 billion to $15 billion beginning in May 2019. The Committee intends to conclude the reduction of its aggregate securities holdings in the System Open Market Account (SOMA) at the end of September 2019. The Committee intends to continue to allow its holdings of agency debt and agency mortgage-backed securities (MBS) to decline, consistent with the aim of holding primarily Treasury securities in the longer run.

Beginning in October 2019, principal payments received from agency debt and agency MBS will be reinvested in Treasury securities subject to a maximum amount of $20 billion per month; any principal payments in excess of that maximum will continue to be reinvested in agency MBS.

Principal payments from agency debt and agency MBS below the $20 billion maximum will initially be invested in Treasury securities across a range of maturities to roughly match the maturity composition of Treasury securities outstanding; the Committee will revisit this reinvestment plan in connection with its deliberations regarding the longer-run composition of the SOMA portfolio.

It continues to be the Committee’s view that limited sales of agency MBS might be warranted in the longer run to reduce or eliminate residual holdings. The timing and pace of any sales would be communicated to the public well in advance.

The average level of reserves after the FOMC has concluded the reduction of its aggregate securities holdings at the end of September will likely still be somewhat above the level of reserves necessary to efficiently and effectively implement monetary policy.

In that case, the Committee currently anticipates that it will likely hold the size of the SOMA portfolio roughly constant for a time. During such a period, persistent gradual increases in currency and other non-reserve liabilities would be accompanied by corresponding gradual declines in reserve balances to a level consistent with efficient and effective implementation of monetary policy.

In case the Fed laid an egg I bought a put option on Wayfair, but quickly sold it after their release for a ~ $40 loss.

Yield on the 10-year looks to be testing 2019 lows. FANG and gold miners are both up a good bit while Virtu is off a couple percent.

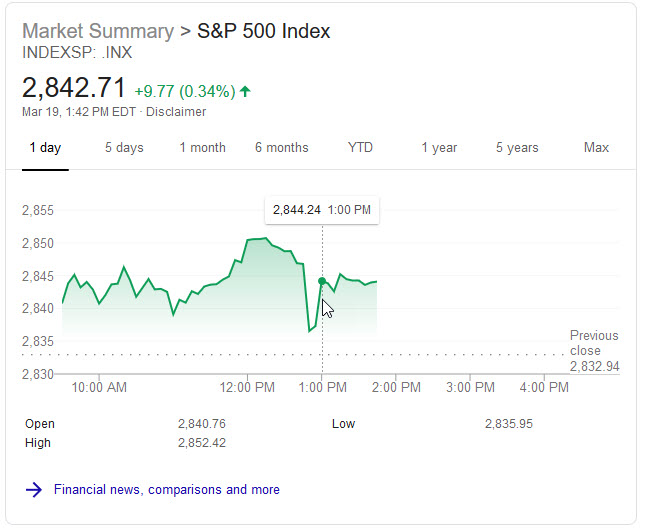

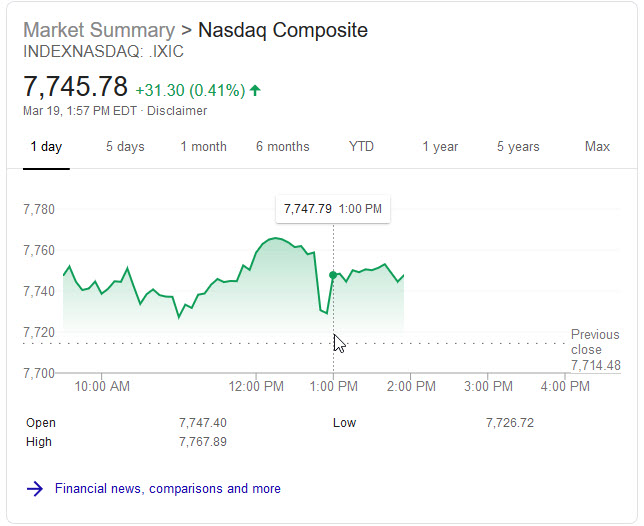

As of writing this the Nasdaq is up about 2/3% while the S&P 500 is up a 3/10% & the DJIA is up about 1/20th a %.

Growth is clearly beating value today. Health stocks were off a bit today. And some value investors are exiting stage left in spite of bond yields falling.

Kroger’s lead director, Robert D. Beyer, who has been on the company’s board since 1999, sold 80,000 Kroger shares on Tuesday for a total of $1.96 million, an average price of $24.52 each. … Beyer’s sale—at a price that represents an 11% loss from the end of 2018—is the biggest sale unrelated to the exercise of stock options by a Kroger insider in six years

By the time the digital ink had dried (was it ever wet?) the market once again traded higher.

And stocks which would be impacted heavily by an escalating trade war like the following groups were up

retailers: Dollar General, Dollar Tree (selling cheap & low margin goods manufactured in China without the supply chain redundancy of a Walmart)

auto manufacturers: Ford, GM (large, complex supply chains)

And then the broader stock indexes were still up on the day other than the Russell 2000.

In the 15 minutes of decline that was enough time to revise the headline on the above article & advertise it sitewide using a red banner & breaking news headline.

Then when the market recovered it was revised once more: Stocks whipsaw on conflicting trade deal reports, Dow now 100 points higher

We are talking a fraction of a percent here.

That is how low volatility is.

A fraction of a percent is enough to drive words like rapidly & whipsaw.

Anyone trading with excessive leverage while being emotionally triggered & responding to the latest “news” headlines is almost guaranteed to lose unless they fade the over-hyped micro stories.

Update: so the market turned down slightly into the close, which is I suppose makes the stuff I exited during the trading day a good call. Right before the close I bought a tiny position in web hosting & email marketing company Endurance International Group (EIGI). They were off 7% on the day & have given up about 75% of the gains they had since the December low. Their market cap is under a billion & they have a bit over a billion in annual revenues. Given their widespread usage amongst hosting customers they’d be a great buy for anyone who wanted to cross sell stuff to webmasters (a parallel to how Square bought Weebly a while back) & I suspect if they fall much further a P/E group would probably buy them out.

One could certainly argue that Amazon.com, Instagram (new checkout feature), Etsy & other such entertainment or shopping destination marketplaces are displacing independent websites. This is true particularly in light of:

I still think domain names & web hosting have a lot of value in the overall structure of the web. Having your own site gives you optionality to change business models or shift what you focus working on. Further, over-reliance on any platform ultimately leads to abuse by said platform.

This is what regular media discovered too late with Facebook.

Or to paraphrase @benedictevans, papers thought they were in the news business. Turns out they were in the printing and delivery business. And when the Internet obviated that industrial advantage, they were stuck.

It is also worth noting the Chinese (or people in the Trump administration) are very good with their timing of rumor releases. With the Federal Reserve meeting today and tomorrow Bloomberg has this story: U.S. Sees China Trade Pushback as Trump Touts Progress.

Chinese officials have shifted their stance because after agreeing to changes to their intellectual-property policies, they haven’t received assurances from the Trump administration that tariffs imposed on their exports would be lifted, two of the people said on condition of anonymity.

Beijing has also stepped back from its initial promises over data protection of pharmaceuticals, didn’t offer details on plans to improve patent linkages, and refused to give ground on data-service issues, one person familiar with the U.S.’s views said. Beijing is trying to bring in wording that would ensure rules in the trade agreement have to comply with Chinese laws, the person added.

One of two things is happening there:

either the Chinese are trying to make the Federal Reserve look politically captured & own by President Trump, or

the Trump administration talks up great progress in between Fed meetings (under-state risk while over-stating upside) & repeatedly puts out some version of this story just ahead of Federal Reserve conferences so that the Federal Reserve owns any market declines.

Either view ends up ascribing more political savvy than most would like to give credit to Xi or Trump, but then you don’t get to lead such a strong country by being an absolute idiot.

Volatility in currency markets is largely nonexistent, at least for now:

With central banks standing pat and little else to drive markets, the betting on low volatility itself is helping to drive trading, says Russell LaScala, Deutsche Bank’s global co-head of foreign exchange trading. He calls the situation “self-perpetuating,” adding that “these loop orders control the market absent any events.”

But this can easily be undone. If an economic or political event leads to a market swing, banks can suddenly forgo their hedging activities, looking to profit from any rise in volatility. That would remove a stabilizing force from the market. At the same time, investors who had bet on low volatility would get burned and rush for protection. That in itself would feed further volatility.

The risk is that the current situation proves similar to one that preceded the big selloff in stocks in January 2018 after a long stretch of ultralow volatility.

What goes up when currency volatility increases? The underlying currency that rises & perhaps a currency hedged equity play in the area where the currency falls, or put options on overly extended high beta stocks. If there is a strong play there with limited holding cost that seems like a nice asymmetric bet at the moment.

The S&P 500 climbed to a five-month high last week, putting the benchmark equity gauge on track for its strongest first quarter since 1998. Meanwhile, U.S. crude oil rose to its highest level since Nov. 12, pushing its early year rebound to almost 30%. … Still, many remain concerned about this year’s rebound. One reason is that assets that are considered safer, such as Treasurys and gold, have also held steady after early year rallies, making it challenging for investors to piece together a clear trend of market momentum. Bond prices and gold often decline when stocks rally, a trend that has historically signaled faith in the economy. … about $60 billion flowed out of global stock funds from the start of the year through March 6, the largest such outflow to begin a year since 2008

As of today’s session, before the close, the UST curve is absolutely ridiculous (again). The 5-year note is now trading almost equal to EFF (effective federal funds) once more, eleven bps less than the 52-week bill. The yield on the 5s is now significantly (4 bps) below the equivalent yield on the 3-month bill. Nominal rates from there down the curve are mere bps off the January 3 lows. This isn’t quite how “dovishness” was supposed to turn out.

The eurodollar futures curve is likewise revisiting the worst case (so far). As these contracts have predicted, LIBOR rates have fallen which doesn’t mean things are getting better. Outer contracts are being bid to prices above those from January 3, which suggests this huge, crucial market is starting to get the sense that “whatever” is going on its effects might alter the long run, too.

I recently read Howard MarksMastering The Market Cycle& it is rich with quotable quotes. One that comes to mind:

in an interconnected, informed world – everything that produces unusual profitability will attract incremental capital until it becomes overcrowded and fully institutionalized, at which point the prospective risk-adjusted return will move toward the mean (or worse). And, correspondingly, things that perform poorly for a while will eventually become so cheap – due to their relative depreciation and the lack of investor interest – that they’ll be primed to outperform. Cycles like these hold the key to success in investing, not trees that everyone is assuming will grow to the sky.

After the extremist attacks at mosques in Christchurch, New Zealand three days ago, we might be off to the races with another round of terrorist garbage fueling more terrorist garbage as it was just reported by the WSJ Dutch police are searching for a gunman from Turkey who killed three people in Utrecht & wounded several others. Should more attacks happen volatility should rise & markets which were up decently today turned south on the news.

In case that terrorst garbage picks up further steam I just bought a LendingTree April put option with a strike price just below market. They’re up about 10% since the 7th & are up about 70% from their lows last December. High beta companies which fueled growth through increased ad spending & competitive acquisitions may see their share prices fall. Of course any decline like that which would be akin to what Quinstreet did might be another earnings report or two away, but anything that has moved 70% in a few months could easily give a bit back should things turn dicey.

The China trade war stuff keeps getting pushed out, with the latest whispered extension going into June, so it can be a fresh memory of a win for the 2020 election. There’s no incentive for Trump to rush it so long as the Fed is on pause & is perceived to own any market correction.

Lu Fang, secretary general of the photovoltaics decision in the China Renewable Energy Society, wrote in an article circulating on mainland social media this month that the country’s cumulative capacity of retired panels would reach up to 70 gigawatts (GW) by 2034.

That is three times the scale of the Three Gorges Dam, the world’s largest hydropower project, by power production.

By 2050 these waste panels would add up to 20 million tonnes, or 2,000 times the weight of the Eiffel Tower, according to Lu.

It is easy to attribute strong returns to one’s own skill & greatness, but any day some crazy event like an earthquake or war could massively tank the markets.

When the stock market goes up broadly momentum stocks work, but then when the market is really strong overall sometimes there isn’t even a lot of sector rotation & anything that falls also gets bid back up.

It certainly looks like the bottom is in on CVS & WBA. Today Bernstein initiated coverage on CVS at outperform, causing the stock to jump over 3 percent. And that is after a couple days of strong performance.

I sold out of a bit of Coca-Cola & Google I have been holding for a while, both at tiny losses. I also sold out of Weyerhaeuser on Monday at a decent gain & went in and out of Kroger a couple times over the past few days during the post-earnings swoon for small gains.

The tough part about the stock market isn’t making small gains repeatedly & winning on average, it is the constant sort of sucking in of attention. There is always another story to read, another topic to think about. And then are you actually learning something that gives you an edge, or are you busy engaging in a game of confirmation bias?

I’ve been reading Howard S. Marks’ Mastering the Market Cycleand it is certainly easy to feel like you are able to see the capitulation stage on stocks like CVS last week (though one can of course catch a falling knife a bit early!), but the broader market is an area that feels a bit less certain to me today.

The broader trend is clearly up right now. But there hasn’t been more than a few days of pullback since the December bottom & it feels like risk is accumulating as price goes up. As of writing this, so far today only 5 stocks in the S&P 500 are down a percent today – that’s opposed to 99 that are up that much or more. The only strong recent pullback is Boeing, but even after the pullback they are still up almost 300% since early 2016.

An escalation of the trade war, another sort of impeachment threat, etc. … the market seems to sort of shake off and ignore these types of stories for now, but any day the response to negative stimuli could turn the other direction.

Sometimes when you see growth stocks go up there is a rotation out of bonds & bond proxy stocks like dividend aristocrats, utilities, telecom, REITs & other assets that are frequently negatively correlated with an up day in the broader market like gold, miner stocks & plays like Virtu. But today almost everything is up.

Smallcap, midcap, or largecap, * value, core, or growth … up up up, up up up, up up up.

Brexit uncertainty in the UK? GBP up, Euro up, UK stock market up, European stock markets up

Commodities up

MercadoLibre announces a secondary stock offering that dilutes existing shareholders 4.7% … stock up 3% on the news. why not?

About the only tangible^ things that are down today are the Dollar, volatility & VIX.

I guess today I’ll deploy patience. I still think CVS has a bit to run, but I will stay mostly in cash until something slides a bit. Better to have a bit of cushion on an entry point rather than doing like I did where I bought Google about a day before the WSJ announced Google had a security issue with Google+ & then before they recovered from that there was the Federal Reserve induced year end swoon driven by the October comment about being a long way from neutral. After the market slid the Fed changed their tune, but that Google stock was dead money for almost a half year.

^ and then there is Pinduodu, the Chinese version of a socialized Groupon 2.0 that slid about 15% today after announcing wider than expected losses. They are still valued at about $30 billion – roughly 15x what Groupon is valued at – so I can’t say I see that one as an opportunity, particularly as they are still losing money & are trading at something like 10 times sales in a low-margin industry. Total pass. Yuck. And – as a bonus – they did a secondary offering last month knowing the results of the quarter they just reported.

Kroger’s quarter bombed on lower sales, lower guidance, and lower profits. A triple lindy trifecta of pure winning.

I traded the dead cat bounce on it for a quick gain. Shares were down about 12.8% when I bought & around 10% when I sold.

“Its shares slid 11.6 percent in morning trade after it also reported a 10 percent fall in fourth-quarter revenue and lower-than-expected earnings for the first time since October 2017. Profits are expected to come under pressure as the retailer plans annual spending of up to $3.2 billion — up from $3 billion last year — to overhaul stores and improve its online business under a program called “Restock Kroger” launched over a year ago.”

The big tech monopolies can basically spend infinite CAPEX and have it get brushed off as justifiably investing in faster growth, while any of the old line slower-growth & lower-margin businesses going through transformation get slaughtered for making similar adjustments to modernize their business to take advantage of the web.

Conceptually, Amazon can consider anything a beta (nixing their pop up shops) & get rewarded for any sort of news / change / noise / speculation, which tells the old line businesses to invest to narrow the competitive gap or at least the narrative gap & then they get killed for it.

Kroger’s digital sales rose 58% during its latest quarter, and the company said it is offering delivery or online pickup at 91% of its stores. … Kroger has pledged to generate $400 million in operating profit by next year, in part by diversifying its sources of revenue. The grocer is pushing into financial services, selling its consumer data to suppliers and selling more ads to target shoppers.

That really shows the power of leading a trend versus following it or trying to play catch up.

Not only do the tech monopolies get the benefit of the doubt, but there are dozens of food delivery startups which lose money on every order, yet they are raising billions.

“Billions of dollars have been spent in a quest to build services that reliably move fresh food from one place to another, yet many in the business wonder if they will ever get the economics right. Most delivery orders remain unprofitable. … Only 1% of 2,874 consumers surveyed by the research firm were willing to pay the full cost of grocery delivery. And 85% of consumers aren’t willing to pay more than $5 for restaurant delivery, according to a recent survey of 2,000 fast-food and fast-casual customers conducted by online ordering platform Tillster. … Venture-capital firms put $5 billion into U.S. food and grocery delivery services last year, more than four times the amount they invested in 2017 … Food sellers pay the services an average fee of 10% to 25% on each order, which means the actual deliveries often lose money. Better placement on the services’ websites or apps costs even more.”

Retailers with a 1% to 3% profit margin aren’t going to win by paying third parties 10% to 25% of each sale.

And as long as humans are needed for deliveries margins will be terrible at third party delivery services. And when automated delivery becomes highly commoditized & widely available, most of the value will bypass any third party delivery services and accrue directly to the retail outlets.

I might consider buying KR again in the future, but the whole market feels like it is sliding down & when the market is sucking an egg you basically have to trade almost perfect on long-only trades to stay flat. Unless you short stocks, you are almost better off ignoring the market until there is an uptrend.

The S&P 500 sliding below the 200-day moving average is not a great thing. Even if that is a nonsense technical signal of limited relevance, the fact that many people follow it makes it real. Many will be selling to de-risk portfolios and keep some dry powder.

CVS is down once again, along with Walgreens Boots Alliance (WBA). At this point both are deep value plays which are priced as though their business models are doomed. If multiple company insiders spent 6 figures on CVS shares at about $58 a share about a week ago, then the current $52 share price doesn’t look particularly expensive.

The three-judge board, appointed by the Librarian of Congress to determine copyright payments, voted 2-1 last year in favor of raising the percentage of mechanical royalties owed to a song’s writers from 10.5 percent of revenue to 15.1 percent of revenue by 2022. The decision followed a two-year trial regarding how songwriter royalty splits might adapt to the streaming era. The leading songwriter association is calling the appeal by tech companies “shameful” and has announced plans to file its own appeal.

Central banks are pouring fuel on the fire as normalization seems to be … err … not working so well.

10 years ago markets made their crisis lows. For 10 years the Fed was "accommodative" For 3 months last year they weren't & everything fell apart. After markets dropped 20% they went back to accommodative by stopping rate hikes. Now they're signaling QE & neg rates. ¯_(ツ)_/¯

The Bank of Japan appears a decade or two ahead of other central banks in their seemingly never-ending interventions. They’ve killed their bond market (as they are the market) & the central bank owns a huge portion of their domestic ETF markets while bond yields are effectively zilch out to about a decade.

China is a firehose of money, seemingly announcing a new stimulus measure almost every week. Lowered reserve requirement ratios, QE-styled stimulus, tax cuts, etc.

The European Central Bank made a major policy reversal Thursday, unveiling plans for fresh measures to stimulate the eurozone’s faltering economy less than three months after phasing out a €2.6 trillion ($2.9 trillion) bond-buying program, making it the first rich-country central bank to ease policy in response to the global slowdown. The ECB said it would hold interest rates at their current levels at least through the end of this year—months longer than previously signaled—and announced plans for a fresh batch of cheap long-term loans for banks.

A $5.7 trillion borrowing binge by U.S. companies could make a slowdown in the world’s biggest economy even more painful and is one more reason the Federal Reserve was wise to put interest rate hikes on hold, Robert Kaplan, president of the Dallas Fed, said.

60 Minutes will soon have a segment with Federal Reserve head Jay Powell this Sunday. It’s probably nothing.

FED'S POWELL TO APPEAR ON CBS'S `60 MINUTES' PROGRAM ON SUNDAY

Preemptive Fed PR campaign ahead of what Draghi & today's USD move just made inevitable? #MrBrownstone

Sector rotation continued yesterday with some emerging market plays like Ctrip up big, bring up other smaller parallel plays like MakeMyTrip. Despegar might be a higher leverage way to play OTAs in emerging markets, though the sort of “national champion” model promoted by China & which India aims to emulate will likely provide a greater level of protection from foreign firms aiming to leverage their current profits from the western world into price dumping to grow to a dominant share in emerging markets.

Funko gave back the pop they had after reporting earnings. They are now trading around where they were before the November stock market sell off.

Since reporting earnings CVS has traded like a penny stock – giving away its quarterly dividend worth of market cap daily for a couple weeks straight. They are off about 22% from February 19th & have fallen by over half since July of 2015.

On way to create a 4% dividend is to start with about a 2% dividend and watch the stock get cut in half. 😀

If the economy goes into a recession there is a fear that Democrats could take both branches of Congress & the presidency, and perhaps initiate some changes which crammed down spending in healthcare. It is worth noting Nancy Pelosi’s top health policy aide told health insurers not to worry about “Medicare for All” impacting their businesses.

Pelosi adviser Wendell Primus detailed five objections to Medicare for All and said that Democrats would be allies to the insurance industry in the fight against single-payer health care. Primus pitched the insurers on supporting Democrats on efforts to shrink drug prices, specifically by backing a number of measures that the pharmaceutical lobby is opposing.

The above approach would seem to lessen the risk of the steep price CVS paid for acquiring Aetna.

Walgreens Boots Alliance has also been careening downward. There was a big multiple percent reversal on CVS yesterday with heavy volume, but then it headed lower once more to close the day & both were down significantly early again today.

There’s a good chance the bottom is in today or tomorrow on both the 2 big drugstore chain stocks unless the entire market tanks – though if that happened it would likely drive investors into defensive sectors like healthcare. Walgreens Boots has debt leverage & more of a global footprint, whereas CVS also has loads of debt due to their Aetna piece which they paid almost their current market cap for. Writing down one acquisition while beginning to integrate a larger acquisition is a great way to crater share prices.

Rite Aid is a proper penny stock with a share price of 66 cents & a market cap around $700 million. That’s quite a fall from their 1999 price of over $50 a share. Their current price isn’t too far from touching their December 2008 prices. They don’t have enough scale to remain relevant.

Target was up big yesterday after reporting earnings & offering strong guidance. After gapping up about $4 a share at open yesterday they are up another $1 today.

Kroger also further recovered from last week’s “oh no Amazon” narrative. Kroger’s almost where they were before the Amazon semi-announcement. That is the second time fading the scary Amazon headline has been a winner for Kroger shareholders.

Target, Kroger & Walmart are quietly fighting back against Amazon.com by becoming online ad plays in their own right.

“Walmart likely has $2 billion to $3 billion in annual digital ad sales already, but could grow that to $5 billion within a couple of years, Stich says. He estimates Amazon ad sales now at $15 billion. And he says that Kroger Co., which only in recent years has developed substantial digital ad revenue from its online grocery business, now has nearly $1 billion in digital ad sales, similar to Target.”

Given the high margins associated with online ads & mass market retailers creating more private label goods to improve margins, differentiate their stock & force ad buys, low margin retailers could see significant margin expansion which offsets delivery costs they ate by trying to adjust their narratives to better compete against Amazon.com. Target has already adopted differential pricing based on user location & is building out a third party network of complimentary suppliers to display on their website.

“Beauty items offer high margins for grocers, and Amazon has expanded its array of such products under various labels. Health and personal-care items are Amazon’s largest source of consumer-product sales online, with roughly $5 billion in sales last year, according to e-commerce data analysts Edge by Ascential. … Though more shopping is expected to migrate online, less than 5% of the roughly $1 trillion in annual U.S. food and consumer product shopping is done over the internet now, market research shows.”

My wife loves the Boots beauty products section in the Walgreens between Westfield mall & Chinatown in SF, so any success by Amazon there is another whack to the pharmaceutical retailers.

Carl Icahn is taking his second blood letting from Dollar Tree. He established a stake in the company last October. On earnings they announced they would close 390 of the Family Dollar Stores they purchased from him & other shareholders for $8.5 billion in 2014.

Barron’s quoted a Needham analyst today who suggested Alphabet should spin out YouTube.

“We believe Netflix (NFLX) is the best public comparable for YouTube…A current Netflix multiple of our estimated YouTube net revenue of $14 billion implies that the value of YouTube is about $140 billion.”

The odds of that happening anytime soon are IMHO approximately between 0 and 0 percent. They could, however, eventually start breaking out reporting of performance much like Amazon did with AWS.

They’ve been hesitant to do that for a couple major reasons

the core click volume of search has been growing slowly as much of the search volume growth is in emerging markets with limited ad coverage. most of the ad click growth Google is reporting is YouTube video ads – particularly the unskippable preroll ads.

they can keep suggesting they are investing in growth with YouTube & it is unprofitable to keep their high 45% take rate on ads from YouTube partners (as opposed to 32% on AdSense) & potentially shield the “unprofitable” service from lawsuits and negative media coverage each time an antivax, suicide tips, or pedo or hate preacher genre is exposed for allegedly playing some outsized roll on the service

One other thing I find at least a bit ironic & hilarious is many news sites are relying on cutting edge Google technology to help moderate their comments.

“Rather than using machine learning to determine what is or isn’t against a given set of rules, Perspective’s challenge is an intensely subjective one: classifying the emotional impact of language.”

Meanwhile YouTube is known for having the singularly worst comments section on the entire web. Recently Google suggested YouTube partners could get demonetized if they did not police comments on their videos.

“instead of hiring more moderators and building better tools to flag abuse, YouTube has, once again, put the responsibility on YouTubers. Now, on top of the burnout-inducing production schedule required to remain in algorithmic favor, the company expects creators to act as their own community moderators.”

Literally anybody can boost their popularity by promoting a viral story about a seedy subsection of YouTube. From the above article:

As part of the backlash against Watson, an old clip from one of his now-private videos is also currently circulating. It’s a scene from a man-on-the-street prank video which allegedly shows Watson asking an underage girl if she wants to make an adult video.”

Why the hell isn’t Google offering the moderation tech as features to their YouTube partners?

In spite of all the media hate YouTube garners, it is a great service which is having profound impacts on millions of lives, especially in emerging markets like India where local substitution will accelerate massively due to cheap access to information.

“There was a time when people had paper maps,” Sengupta says. “Today you walk around India and see everyone using Google Maps because they work off-line.”

…

“Several Saathis and their trainees have seized the chance to start cottage industries with their new Internet skills, downloading instructional videos on YouTube on how to make homemade honey or embroider shirts, for example.”

Funko reported a strong quarter with sales jumping 38% YoY to $233 million in the 4th quarter. Their stock is back above $21 a share, giving them a market cap above a billion & having the stock roughly double off the December lows. They are opening a Hollywood store to boost brand awareness, are projecting YoY growth rates of 18% to 20% (above expectations) on top of the beat & are growing into the board games category through their recent acquisition of Forrest-Pruzan Creative.

The fact that Fortnite, which the Washington Post called “the biggest pop culture phenomenon of 2018” accounted for only 12% of our Q4 sales and 5% for the year, showcases how Funko is like an index fund of pop culture. The property is important, but it’s just one of many in our portfolio. Evergreen properties accounted for about 46% of our sales in Q4 and 47% for the full year. Again, this shows that we’re not reliant on a small number of hits, nor are we reliant on only new content

Funko President Andrew Perlmutter

Grocery Stores

Grocery store stocks once again sold off on news Amazon will attack the category by launching another line of grocery stores.

eBay

eBay added 2 board members from activist investors Elliot Management Corp. & Starboard Value.

China Doom Machine

Kyle Bass was once again interviewed on Real Vision. He mentioned how capital left China in a variety of formats including loans in foreign currencies not paid back, diamond sales, cryptocurrencies, etc. & how those generally happened in waves until they got shot down by regulators.

LendingTree is up to $322.60 from a December 24 low of $200.05, a gain of over 60% since the market bottomed. They are now valued at over $4 billion. A large part of their growth has been based on acquisitions.

Their core business has seen growth through aggressive expansion of their Google Ads / AdWords ad campaigns.

Through the next 3 to 6 months that ad spend will still provide additional growth, but it looks like the ad spend has flattened over the past couple months, so in about 9 months that ad spend will be required to maintain share rather than buy growth. Some of their other acquisitions like ValuePenguin rely more on organic exposure, while it appears MagnifyMoney has been fairly flat on Google Ads spend & DepositAccounts.com has ramped up their Google Ads spend over the past half-year.

Outside of CompareCards.com (which has a similar Google Ads chart to the above LendingTree chart) most of their secondary sites are generally far more reliant on organic search than their main site.

When you look at the acquisitions we’ve made, they’ve all been people who are in kind of the same business we’re in, albeit, in some cases, more SEO-oriented. Our SEO strategic initiative was because we knew that we were under-indexed there from a marketing perspective. And the combination of Magnify, Deposit and now ValuePenguin, we feel like we’ve built and will continue to build organically an SEO business. But I would not anticipate more SEO-oriented acquisitions, okay? We feel like we’ve achieved that strategic objective.

J. D. Moriarty

They also mentioned growth rates of specific properties:

We’re also beginning to see real traction in SEO with meaningful growth across multiple brands and product categories. DepositAccounts and MagnifyMoney have both doubled their revenue since we acquired the brands in 2017. And through our centralized SEO function, we’re becoming a scale player in the content transaction model space.

Our investment in off-line advertising is also resulting in lift across a number of channels, including direct traffic, branded SEM and SEO. We’re seeing a 40% year-over-year increase in direct-to-site loan requests, a 43% lift in branded SEM loan requests and a 17% increase in loan requests from SEO channels.

Last year when LendingTree was close to their peak I bought some put options that turned out ok. If I were broadly long the market now I would be tempted to consider buying a few LendingTree put options or maybe some put options on Wayfair. On the conference call LendingTree mentioned their My LendingTree platform could see strong growth due to cross-marketing of higher payout credit card offers.

I think UBS Investment Bank’s Eric Edmund Wasserstrom gets at the core issue with the market size opportunity & growth drivers at their elevated P/E ratio.

I guess what I’m ultimately trying to discern is, on the one hand, the recent drivers of guidance upside have come largely from acquisition integration. And at the same time, it looks like within the core business, there’s an increase in marketing and acquisition costs. And so I guess what I’m trying to understand is, has there been some change here wherein organic growth is just becoming more challenging and, therefore, more expensive to accomplish? And is that some indication of kind of the go-forward economics of LendingTree’s business?

LendingTree has held up quite well when compared against the likes of QuinStreet, which has slid from $20.02 to $13.60 a share after a weak Q4. No doubt LendingTree is a stronger business, but then there is also a huge gap between trading at around a 10x multiple or trading at about a 50x multiple.

The lens through which you have experienced the world is also the lens through which you ultimately view the world. Thus a person who spent decades in marketing could argue that almost everything is a subset of marketing. But sometimes it becomes a bit of a reach.

Last year I read Ken Auletta’s Frenemiesbook which detailed how technology was changing the media landscape & impacting ad agencies. One of the companies repeatedly featured in the book for taking innovative new approaches to marketing & promoting their brand as being cutting-edge was GE. They currently trade at about $10 a share, down from about $30 a share a couple years ago when the book was being researched.

Intel had built an in-house ad agency, was building dancing robots, etc. … and in the process let TSMC get ahead of them in being able to produce chips with transistors at a 7 nanometer density while Intel is still at 10.

Kraft Heinz recently slid 27.5% after missing their estimates & slashing their dividend. They wrote down the value of their Kraft & Oscar Mayer trademarks by $15.4 billion. After years of 3G’s zero-based budgeting they failed to keep up with changing consumer tastes. It is hard to sustainably cut your way to success.

Other than accounting, it seems they have no idea what they are doing.

“I’m a terrified dinosaur. I’ve been living in this cozy world of old brands [and] big volumes. You could just focus on being very efficient and you’d be OK. All of a sudden we are being disrupted in all ways. We bought brands and we thought they would last forever. Now, we have to totally adjust to new demands from clients.”

Last May Warren Buffett mentioned the ongoing battle between brands & private label brands offered by retailers.

Barrons published an article mentioning the direct-to-consumer trend could drive ad growth for Google & Facebook.

“As direct-to-consume brands become more confident in their ability to drive repeat business organically,” he wrote, “we believe the willingness to pay for the initial customer acquisition naturally grows, which could serve to continue to grow ad revenue derived from these verticals over time.”

After under-funding growth for long enough, cutting the business to the bone, the only solution is … divestures. Maxwell House is one of many brands which is up for sale.

Mood at the company, which saw its shares plummet nearly 30 percent on Friday, is dour, say people familiar. It is taking a no stone unturned approach to which brands it should or could unload, they say.

In the age of the #MeToo movement & all the spiels about “brand safety” in the advertising world one would have to be utterly tone deaf to broader cultural trends to run such an ad campaign. There’s no way a risk-adverse roll up play consisting of old line brands intentionally creates custom ad campaigns targeting porn unless they are desperate.

When a company starts running cutting-edge ad campaigns on Pornhub or introduces their version of Shingy, they may not yet be a short (after all, subpar performance can be announced with increase share buybacks or a company can position itself for buyout to only later become a writedown by the acquirer) but buying out of the money put options ahead of earnings releases might not be a bad idea.