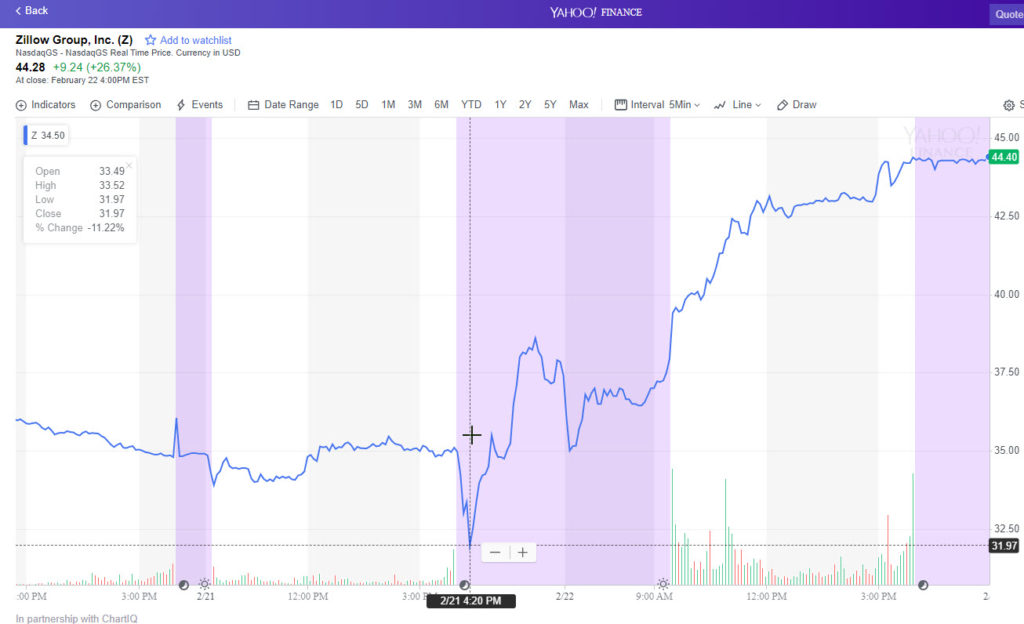

For the past couple quarters Zillow has slid after reporting quarterly results. The big themes on the slide were the erosion in the growth rate of their core business (selling ads to Realtors) coupled with new (perceived?) risks to their business from adding new business lines including lending and home flipping.

In after hours on the most recent quarter the stock immediately slid after reporting results, with the stock falling nearly 10% from $34.97 a share to $31.97. The stock then quickly reversed course, ending after hours at $37.94 & closing out the next day up an additional 26.37% during trade to end at $44.28 a share.

When I up, down, touch the ground, puts me in the mood, in the mood, for food – Winnie the Pooh

A quarter ago when Zillow announced results Jim Cramer mentioned how such a stock could torpedo a portfolio, they could still have a lot of downside & how the desperation among the company was “unbecoming.”

I am not surprised they jumped on the announcement they were changing CEOs back to Rich Barton & were aiming to create an extra $20 billion in revenues within 5 years by flipping up to 5,000 homes a month.

Even after the recent huge 35%+ swing in share price, Zillow is still valued at about $9 billion. At some point it would even make sense for someone like Massa to jump in and buy Zillow shares to maintain narrative control over his large investments in Opendoor. It is hard to claim the over $1 billion invested into Opendoor with a valuation now around $3.7 billion is rational if Zillow (which is the dominant player in the category) is only worth around $6 billion & jumping into the home flipping category is considered value eroding for Zillow.

If you had to create Zillow again from scratch you probably couldn’t, as such an effort would almost certainly get hit by the Google Panda algorithm. Further, Realtor.com, their most direct competitor in the search results, isn’t really closing the gap.

If you do the math on the home flipping, it is a lot of revenues, but is not a lot of profits. From a few recent interviews I have read, it sounds like Zillow is mostly interested in light-touch quick flips, and while that strategy certainly limits downside risk, there is also a limit to the size of the market & the profit potential in that market. In Q4 of last year Zillow made $1,723 in profit on the 141 homes it sold.

Zillow paid $264,134 on average per home it sold in the quarter, and spent over $20,000 per home on renovation and selling costs. Once interest and holding costs were taken into account, Zillow’s cost per home was $291,518 per home, meaning the $293,241 in revenue it generated per sale amounted to a 0.5% profit margin. Earlier in the year, when housing activity was stronger, Zillow appears to have generated more than twice the margin.

As Zillow and other iBuyer competitors scale up the home flipping business, they may be able to increase capacity utilization, but they likely will drive down margins on the business unless they go into tougher projects (greater risk + longer turnover times) and perhaps decide that their core business model is strong enough that they can afford risking pissing off Realtors and squeezing them out of the conversion process on their owned inventory.

I think most penny stocks are penny stocks for a reason – either they are failed businesses, scams, or have some other reason they remain publicly traded while having little to no economic value (based on their market price).

In some cases regulatory changes can cause formerly broken businesses to become once again viable. That is what some people are betting on with Fannie Mae (FNMA) & Freddie Mac (FMCC).

GSEs up up & away

However, most penny stocks never break out of the category, or only do so for a scarce & fleeting bit of time. As much capital as there is in the world, if a penny stock had some sort of powerful strategic advantage it would in most cases quickly go private.

One penny stock I was curious about, but ultimately never touched, was Health Warehouse (HEWA). They currently trade at 32 cents a share & are valued at about $15.6 million.

They had absolutely fantastic rankings in Google about a year ago. The month their organic rankings fell off so did their stock price, giving up about half its value.

The reason I never bought any of their stock is the thing seemed so illiquid you would end up moving the market cap 10% or 20% if you were to invest enough in it for the returns to count for anything. And then if you thought you could boost the rankings of their property you would also have to invest quite a bit again, so it is something where you would probably need to invest about 6 figures into in order to see a worthwhile return, but that is a big chunk of change to put in a penny stock.

And the tough thing with search is the trend isn’t really your friend & no matter what your best efforts are, if an algorithm update moves against a site it can more than undo any work you’ve done.

“Google can’t help but being predatory in saying, well, you used to get all this traffic for free, our goal, over the last, now it’s about 10 years, has been to say, no, traffic is not going to be free. Those 10 blue links you used to see are now disappearing, so below the fold”

If your point of leverage & potential high returns come from the fact that you are overly indexed to the online ecosystem, any change in one of the core players can cause a steep decline in growth rates, sales volume, leverage with suppliers & profit margins. And online-only plays are ultimately playing against the clock as their offline analogs slowly adopt best practices to compete online.

Last year’s sell off was relentless. Even trades that had long bases & were overly obvious still cratered with the broader market. No matter what you were in, if you were in almost anything (other than a short position) you were virtually guaranteed to lose as asset prices deflated.

Up, up, up since December 24th.

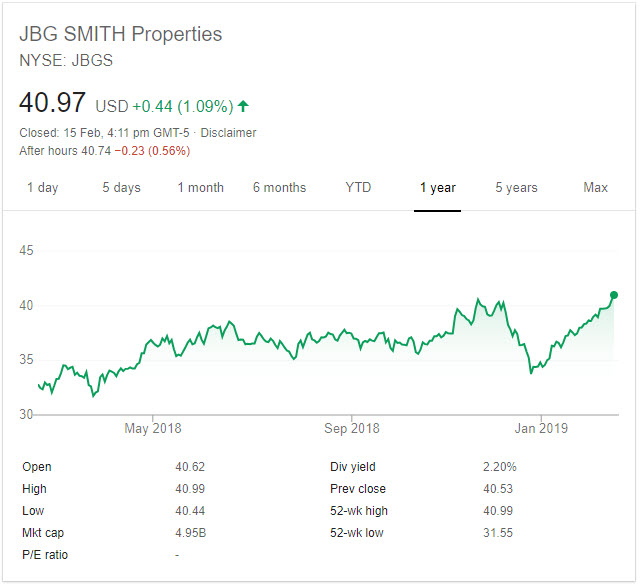

Amazon.com announced they were nixing their New York City HQ2, and would grow their other locations instead. JBG Smith Properties (JBGS) instantly jumped on the news & is making fresh all-time highs.

Since December 24th much of the market has seen a relentless bid higher. Enterprise software is up, game makers up even after weak performance, REITs & many other bond proxies near 52-week highs, gold strong even as the Dollar has been strong, oil prices recovering, the Nasdaq has entered a new bull market, etc.

On Dec 24, only 1% of stocks in the S&P 500 closed above their 50-day moving avg, one of the most extreme oversold levels in history.

After an 18% vertical rally over the last 8 weeks, that number now stands at 92%, one of the most extreme overbought levels in history.$SPXpic.twitter.com/hx3vm3Jj2e

Even some companies which reported strong results have seen shares slide. Yandex (YNDX) slid 8.54% yesterday & their conference call didn’t sound particularly horrible. Their ride sharing is already profitable if you back out self-driving & food delivery, they are likely to benefit from the hype cycle around the Lyft & Uber IPOs, they are still projecting search revenue increases of 18% to 20% this year, and while they saw rising TAC it was due in part to them gaining search marketshare on Android devices.

The above being stated, Yandex was as low as $24.90 on October 19 last year on rumor they could get acquired by Sberbank & they are now down to $31.47, so that is still a big 26.4% jump off those lows.

Part of the recent bullishness is alleged positive trade talks with China. But ultimately Trump has zero incentive to quickly solve the trade war stuff, because once it is over & people do not have some gain to look forward to & they realize their lives haven’t improved much he can’t use that narrative to drive re-election. So he is going to have to drag the trade war stuff out for at least another year & some of that will be via significant headline risk.

Now there is sort of a bullish mindset across the markets & maybe it holds, but I recently bought a bit of Virtu (VIRT) in case it doesn’t & those sort of one-off edge case slides start to spread throughout the market.

If I am correct, I suspect we will see many Democrat candidates (perhaps all?) adopt MMT as a tenant of their platform. And here is a crazy thought for you – what if Trump beats them to it?

…

Although I don’t have any concern about the government funding itself, I do have lots of worry that inflation would quickly rise and before too long, the government would be forced to cut back its spending, and that typical of governments, it would prove much more difficult than instituting spending. Therefore I would expect fixed-income to be a terrible investment under MMT. Even if the government pegs rates low, inflation will be the real risk. It would make little sense to sit in an asset that pays fixed.

Foreigners sold $77.35 billion in U.S. Treasuries in the month, after net sales of $13.2 billion in November. December’s outflow was the largest since the U.S. government agency started recording Treasury debt transactions in January 1978.

“I think the Fed is going to change that policy subtly over time,” Dudley said. “They are going to talk about, ‘We want to hit 2 percent inflation on average.’ And that’s going to imply to people that if they miss on the low side for a while, that they’ll be willing to miss on the high side for a while.” – former New York Fed President William Dudley

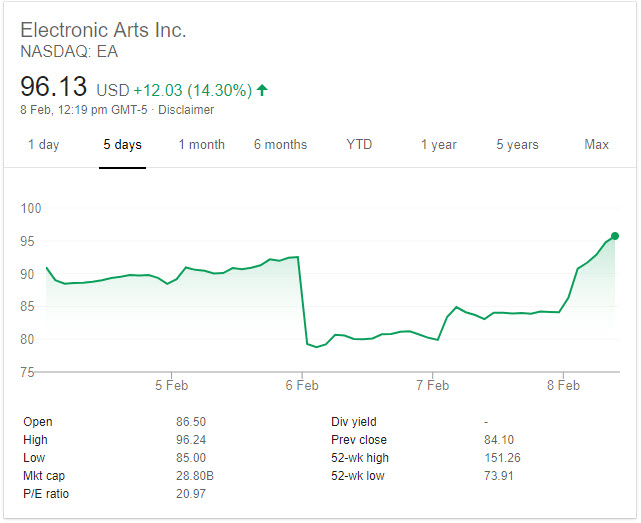

So much for the game market being destroyed. Two days later and it is as if the poor quarter from EA never even happened.

Eh? What Bad quarterly earnings report do you speak of?

Activision (ATVI) hasn’t recovered anywhere near the degree EA did, Nintendo (NTDOY) is not far from 52-week lows, Take Two Interactive (TTWO) hasn’t regained much of what they lost & NetEase (NTES) is still off big.

Gaming company stocks after EA quarterly results announcement.

Yesterday after the adverse market reaction to the Kudlow US – China trade war news coverage I saw XOM was down almost 2%, so I bought a chunk of it as today it went ex-div. I sold that shortly after open today for about a half a percent loss BUT about a percent gain in the quarterly dividend payment that will be paid in a month, so it was net up a half percent on a decent sized position. It was a good thing I sold when I did as it has been down, down, down since open & looks like it could slide below $73 today if the market doesn’t turn up soon (edit: yup, it did, $72 & change).

I was also holding a bit of FNKO that I sold for a small gain this morning.

I still have a small position in Nintedo that is off a bit over 3%, but made a similar amount from going in and out of EA & ATVI a couple times. I suspect whenever Google launches the next version of their Switch they’ll get a bit of a bump. I still have a position in Google along with a bit of Disney & Apple that were purchased about a year back.

I’m quite glad to be mostly in cash while the market is choppy, another U.S. federal government shutdown could start next Friday, and the March 1st trade war deadline is only 3 weeks away.

Quinstreet is off about 20% today after meeting expectations . They saw weakness in their core legacy markets of online education (secular declines as the for-profit colleges are ultimately displaced by the nonprofit universities who have partnered with entities like 2U & they lost a large client in Dream Center Education Holdings which is going through restructuring) and home loans (cyclical market softness in response to rising rates hitting refi demand), but saw stronger growth in their other verticals including insurance, credit cards, personal loans, banking, home services & B2B. On the quarter they grew revenues YoY by 19% to $104.1 million. Financial services is 71% of revenues. Education is down to 16% of their revenues. Their recently acquired AmOne personal loan business (which they paid $20.3 million for plus earn out of up to an additional $8 million) is within striking distance of being their #2 revenue driver behind auto insurance. Almost a year ago Kerrisdale Capital Management published an article on SeekingAlpha highlighting how there is a lot of ingredients in the insurance leads sausage.

EA turned in a weak quarter, which caused their stock to slide 15% & also hit Activision / Blizzard for a 10% decline while the Nintendo ADR was off 6%.

I traded in and out of both EA & ATVI for quick small gains & am holding a bit of Nintendo + Activision / Blizzard. ATVI is now below the December 24 lows.

There was a recent Business Insider article which talked about how big of a struggle Nintendo has with their reliance on first-party titles.

“Microsoft and Sony rely on major third-party games like “Grand Theft Auto” and “Call of Duty” to bolster sales of the Xbox One and PlayStation 4 consoles, and only produce a handful of major first-party games themselves. … Just about 85% of Nintendo Switch software sales are first-party games — games made and/or published by Nintendo.”

I believe their analysis is exactly backward. Nintendo’s revenue stream being highly differentiated is a point of strength.

On the most recent earnings call Google’s Sundar Pichai answered a question about the Google Play store 30% rake as though the question was specifically about distributing games.

On Google Play, obviously, we do this at scale, thousands of developers rely on it to safely and seamlessly distribute their games to billions of Android users worldwide. And we invest a lot in our infrastructure to continuously make sure their overall experience is safe and results in high engagement and for the developer’s back. So I think there’s a value exchange there and it’s been the industry standard. And so, I think we will continue down that path but obviously always adapt to where the market is.

If tech companies are displacing the roll of publishers by eating into the longtail of games & taking a fat rake off the top, then whoever has the most differentiated revenue stream has the strongest revenue stream.

If a single strong game can be leveraged into an online game distribution platform, there’s no reason the company with the best gaming IP wouldn’t be able to the same, or to be able to demand a higher revenue share from any third party platforms their content is distributed on.

There are a limited number of broad-based verticals the big tech companies can charge recurring subscription fees for: TV & movie, music, productivity software, hosting & file backups, games…and not a lot else. There are subscription services for books or audiobooks, but they are tiny.

Tech, telecom & other media companies have invested heavily in video streaming services, ultimately creating a bubble where they have doubled content costs for scripted animation & some highly demanded animators are turning down hundreds of millions of dollars worth of demand.

Spotify acquired podcasting company Gimlet Media for $230 million & they also acquired Anchor.

Consumers spend roughly the same amount of time on video as they do on audio. Video is about a trillion dollar market. And the music and radio industry is worth around a hundred billion dollars. I always come back to the same question: Are our eyes really worth 10 times more than our ears?

What will drive Spotify’s growth? Unique, differentiated content.

Our podcast users spend almost twice the time on the platform, and spend even more time listening to music. We have also seen that by having unique programming, people who previously thought Spotify was not right for them will give it a try.

The New York Times hit fresh 52-week highs (13-year highs) after beating revenue & earnings expectations, growing their digital subscriptions quicker than anticipated & raising their dividend 25%.

They have differentiated content & drive the news agenda.

The media industry has already shed more than 1,000 jobs this year, but the Times said Wednesday that it added 120 employees to its newsroom last year to bring the total number of journalists to 1,600, the largest staff in the paper’s history.

NYT might be a great short if Democrats win the presidency in 2020 & their base has less to be outraged by (as their own party is in power). If Democrats are in control there is almost no chance the New York Times will reach their 2025 subscriber goal of 10 million active subscribers.

January was the best opening month for the stock market since 1987. I doubt we will see a repeat of Black Monday with the DJIA off 22.6% in a day, but there are still many potential negative catalysts in the market: debt build up, slowing growth globally, growing political populism & nationalism, trade imbalances across Europe creating ongoing issues, and the trade war between the US and China.

The market may have over-read the Fed’s willingness to hike into a deteriorating market as they lifted rates on December 19th & Jerome Powell stated rates were a long way from neutral on October 3rd of last year. The market might now also be over-reading into Federal Reserve dovishness.

The end of last year was so choppy because there were both tax loss harvesting driving down the price of losing positions & some winners were sold to lock in profits while offsetting tax loss harvesting. Combine those with fear of a hawkish Fed & there were many people with an incentive to sell & algorithmic players riding along to cause heavy moves in a time of year that traditionally has light volume.

We’re at the point where many people who traded on the (incorrect) thinking the Fed would be dovish on the 19th of December now see many of those positions back in the black. I sold out the bigger stake I had in Apple (still have a smaller stake from long ago), the ExxonMobil position I had, the remaining AbbVie I had, etc.

I also dead cat bounce traded Verizon & AT&T on their sour earnings reports, along with Paypal’s fall after reporting earnings. A few days back Funko was off over 8%, so I traded a bit of that & sold it when they were back to off 4%.

Verizon wrote down $4.6 billion – about half the purchase price of Yahoo! & AOL (formerly known as Oath, known as Verizon Media Group after Tim Armstrong left the company). Yahoo! Finance finally launched their subscription offering with a free trial & a $49 monthly recurring fee. Many traditional newspaper chains & upstart online publishers like Buzzfeed & Vice have done rounds of layoffs, so it remains to be seen if Yahoo! Finance has enough pull to be worthy of a monthly subscription years after they shifted from offering lots of original content to mostly referring traffic to third party sites with original news coverage. One thing Yahoo! has going for them is Google gutted Google Finance over a year ago.

One problem with a market that keeps going up is it can allow a speculator to presume they are brilliant because they keep winning on every trade. In a market with bullish sentiment even bad news only temporarily clips stock prices.

After a healthy run in the markets I prefer to have lower exposure so I don’t have big positions caught offsides if any of the big issues crop up & cause dislocations: hard Brexit, Italian politics in Europe, the yellow jackets in France, the tsunami of bad debts in China, trade war stuff, etc. … I’d rather wait for company specific, sector specific or marketwide slides before deploying much capital.

Housing has many headwinds: the TCJA capping SALT deductions, affordability (particularly in a rising rate environment), lower investment from Chinese investors, slowing economic growth, still rapidly rising healthcare costs ramping local property tax payments, uncertainty with potential policy changes toward Fannie Mae & Freddie Mac, etc.

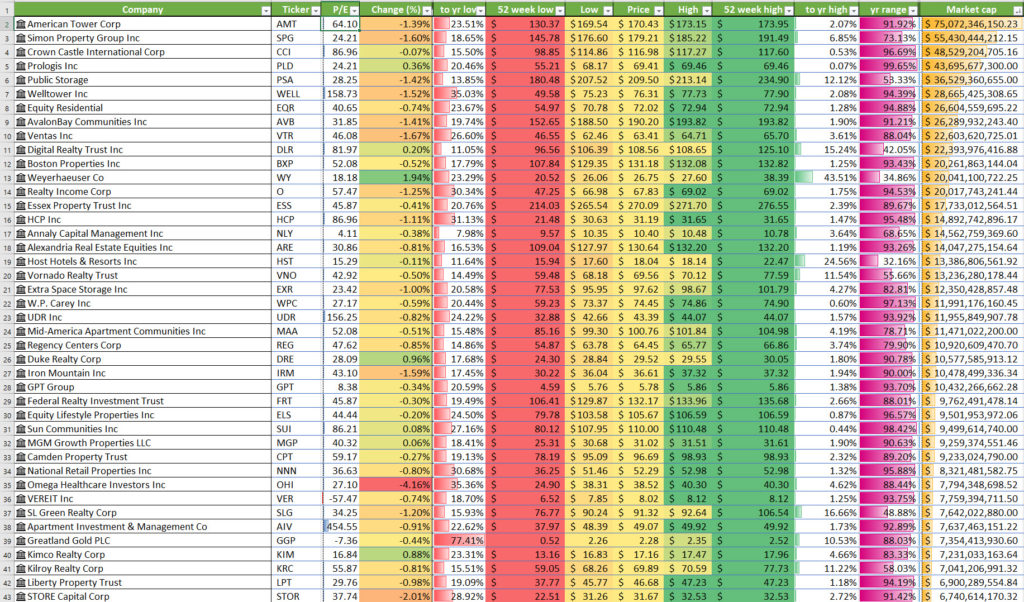

Weyerhaeuser (WY), a timber REIT, was down to $25 a share in pre-market after missing their numbers top & bottom line, during the day they reversed & closed at $26.75, up 1.94% on the day – about a 6% swing from the bottom. They were one of the biggest dogs in last year’s decline, but they’re up over 30% off their lows. They are one of a few large REITs which is not near or at 52-week highs. From the following table you can see in the column one from the right how most of the REITs are within the top 10% of the range they have traded over the past 52-weeks & the column left of it shows most are within 2% to 3% of their 52-week highs.

A Sample of Large US REITs

I bought tiny positions in VLO & TGT today. Both were down significantly on the day. VLO has recovered quite a bit since the Christmas eve bottom in the stock market, but they’ve also seen insider buying & they’ve beat expectations by a wide margin.

As long as diesel margins remain high — and there’s little reason to see them falling, given low inventories — then refiners can live with weakness in gasoline. Valero, in particular, has demonstrated its ability to capture opportunities on margins where it can find them, and pay out any windfalls to shareholders. Conversely, such financial strength means gasoline supply could stay strong as the year progresses.

Tons of retail stocks slid in tandem with Amazon.com after Amazon.com gave soft forward guidance, but some of the issues Amazon is facing like mounting regulatory pressures in India are not being felt by purely domestic US retailers. Amazon facing headwinds in an emerging market likely increases the value of retailers with a heavy United States emphasis, because the US-based retailer does not need to jump through hoops to undo those malinvestments & they can focus on improving their core business, while the multinational has to give more thought to how they are fueling international growth & if it makes as much sense to cross-subsidize into emerging markets where any success will likely be met with a row of nails thrown under their tires.

“The secretary of India’s Telecommunications Department, Aruna Sundararajan, last week told a gathering of Indian startups in a closed-door meeting in the tech hub of Bangalore that the government will introduce a “national champion” policy “very soon” to encourage the rise of Indian companies, according to a person familiar with the matter. She said Indian policy makers had noted the success of China’s internet giants, Alibaba Group Holding Ltd. and Tencent Holdings Ltd.”

Target is only worth a little more than double what Walmart paid for Flipkart. Relative to the market caps of the big tech monopolies both Target & Kroger would be cheap buys if the other big tech players wanted to compete head on with Amazon.com. As Amazon.com becomes an ad farm Google spending less than half of their cash on hand to buy out the largest grocery chain & the biggest broad-based US retailer not named Walmart would be a smart strategy to ensure their conversion process is as smooth as possible & they take the fight to Amazon rather than watching Amazon keep encroaching on their turf.

AbbVie missed earnings estimates on the top & bottom line, causing their stock to slide over 6% Friday. I traded in and out of it 3 times for small gains & still have a position in them going forward.

President Trump signed a bill re-opening the federal government for 3 weeks, which should help relieve some of the short term concerns in the market. China is engaging in stealth QE & the Federal Reserve floated a trial balloon for ending their balance sheet run off far sooner than most anticipated. The Dow Jones Industrial Average, Nasdaq, S&P 500 & the Russell 2000 Index were all up 3/4% or more on the day, which makes the recent decline in AbbVie stand out even more. ABBV is down over 10% so far this year while the broader market is up 6% to 7%, offsetting some of the steep declines seen in December.

Longer term I am iffy on the healthcare industry, as at some point it becomes such a drag on the domestic economy it could literally blow up the global economy.

“In 2018, Americans spent nearly $1.2 trillion on hospital care, representing approximately $9,200 for the median household, or 14.7 percent of median household income. That exceeds what the average family paid in federal income and payroll taxes. By 2026, projected hospital spending will exceed $13,000 per household: nearly one-fifth of household income.”

I traded out of ABBV three times Friday & closed the day with a position up slightly, expecting it to go up Monday. If it gains a few percent right away I might sell it, but if it is a slow grind I am fine holding it for at least a few months. And once I get clarity on some other things I am working on it probably wouldn’t be a name I would mind holding longterm.

TGT stock trades around where it was in July of 2007. In the decade plus since many specialty retailers have went under, been bought out by private equity, or have been bought out by private equity then went under. Every time a company like Toys R Us disappears it ultimately increases the value of Walmart, Target & Amazon.com.

Certain segments of the consumer dollar are relatively slow move online. This is a big part of why Amazon.com bought Whole Foods. Get great urban retail locations & own a slice of the market that seems not to be coming online very quickly. Walmart & Target also have large grocery businesses.

As time passes & Amazon has grown more dominant in ecommerce they have been able to turn their product search result pages into sort of a spam empire. First there’s a big banner ad, then there is another layer of ads, then there is a layer of private label products which eats up the rest of the above the fold screen space and forces brands to buy paid ads in addition to all the other fees Amazon charges (warehousing, logistics expenses, payment processing, etc.)

Amazon is the fastest growing scaled online ad network. And they are taking their profits & investing them into selling Fire sticks at or below cost, video game streaming via Twitch, IMdB Freedive, etc.

As they grow, they are also unveiling new ad features.

“New-to-brand metrics determine whether an ad-attributed purchase was made by an existing customer or one buying a brand’s product on Amazon for the first time over the prior year. With new-to-brand, advertisers receive campaign performance metrics such as total new-to-brand purchases and sales, new-to-brand purchase rate, and cost per new-to-brand customer.”

That feature allows Amazon to over-state its own contribution to the conversion process. They will claim a customer is new to a brand if that customer had never bought that brand ON AMAZON.COM in the past year. This is a similar sort of self-over-attribution as what Google Analytics did with last click attribution over-crediting Google.com for conversions. Or like Facebook did with all their fake metrics on video views & how they give themselves a 28-day window for app install attribution after an ad click.

Part of making a lot of money with an ad network is the ability to not only drive attention, but the ability to over-claim conversion contribution to justify ever-increasing ad spend. Some data is shown, some is withheld. The selective display of data allows the aggregator platforms to give themselves an A+ in terms of ad spend ROI while also keeping partners reliant on them for further exposure.

The more ad networks you spend on in parallel the harder it is to untangle what drove what as everybody wants to overclaim their contribution to the conversion.

If large retailers run low margin businesses pushing 10s or 100s of billions of dollars in product each year & see piles of high margin ad revenues available, at some point it makes sense for them to aggressively compete against Google rather than relying on Google. And they won’t catch up to Amazon on the ad revenue front if they are reliant on a third party like Google for managing their ad inventory.

If Google Express lost Target they’d have major product gaps. And Apple Pay is rolling out widely. So long as all the major platforms are balkanized (be it video streaming, video game stores, cloud computing services, ads, ecommerce marketplaces, operating systems, payment platforms, etc.) then at some point to be more efficient Google will need an internal customer which provides the baseline level of service quality to handle retail logistics profitably. Google Express has went nowhere and only seems to be falling further behind Amazon.com in the US, let alone the sort of amazing stuff Amazon.com is doing in India.

“The Seattle giant has modified its app to work with inexpensive smartphones and patchy cellular networks. It has added hundreds of thousands of Indian language descriptions of products and videos for those who can’t read, and it has opened physical Amazon stores to walk people through the process of ordering online. It brought on tens of thousands of local distributors to deliver packages, often by bicycle down dirt roads, where it will accept cash or digital payment on delivery.” … “Seated at linked computer screens, the customers, most of whom aren’t comfortable with English or typing, can follow along as he pulls up options. He helps them pick the right size using a chart on the wall and a foot measuring device. Later, customers come back to pick up their orders and pay cash at the store. There is even a changing room so they can try on clothes before paying. “It helps me introduce people to the strange new world of the internet, where they can buy everything, try it and even return it,” said Mr. Arjun. He gets an 8%-10% commission on sales. … Humans translated descriptions for 35,000 of Amazon’s most popular products into Hindi. That allowed a machine-learning system to master the language, and eventually every product description will be translated. Amazon said it plans to add voice searches and descriptions in other major Indian languages.”

Google is going to keep getting clipped by the EU, so they probably wouldn’t want to acquire an eBay anytime soon, as they still wouldn’t solve their logistics problems AND they would open themselves up to another wave of fines from Margrethe Vestager.

Target is one of the few US retailers with a broad range of products & a broad base of stores. Other than them and Walmart, who else could Google acquire to finally be competitive against Amazon in ecommerce & local delivery in a game where Walmart is opting out of partnering with Google?

I haven’t bought any Target yet, but if the market heads south for a bit I wouldn’t mind establishing a position that was a bit set-and-forget for a couple years.

PetMed Express reported earnings which missed on both the top line & bottom line, causing their shares to fall about 12% in pre-market trade.

Almost immediately after the market opened up shares ramped up hard in a bull trap, which had shares up above $23 each within 45 minutes of open. They were only down a little over a percent at the peak, while the broader stock market was also down a similar amount. And then the share price slid like a rock until 12:30 PM, bottoming at $20.25 a share.

I wanted to trade the initial ramp, but knew it would eventually turn back, so I sat on my hands until after the stock bottomed & started turning up. I put on a dead cat bounce trade when it was about $20.6 a share, though I got a crappy fill at about $20.83 a share. I looked away from the market for about an hour, came back & saw shares at $21.28, so I sold at market, which was executed at $21.2346, for a gain of about $580 on 1,500 shares.

The company has no debt, $93.2 million in cash, $32.2 million in inventory, a 5.16% dividend yield and a market cap of about $432 million. They’d be a great buy for someone like Mars who perhaps wanted to own a slice of online distribution to limit the negotiation leverage of Chewy.

Back out their inventory & cash on hand and that shaves over a quarter off their absurdly low P/E ratio.

They are no longer a growth story as about 90% of their orders are repeat customers.

Reorder sales increased by 4.6% to $53.3 million for the quarter compared to reorder sales of $50.9 million for the same quarter the prior year. For the 9 months, the reorder sales increased by 9% to $185.9 million compared to $170.5 million for the same period a year ago. New order sales decreased by 26% to $6.8 million for the quarter compared to $9.2 million for the same period the prior year.

Newer customers have been harder to find online as the size of ads in the search results has increased dramatically over the past couple years, lowering the relative value of organic rankings in the vertical. Ad prices have went up as well, and they’ve sort of sat on their hands with a relatively flat ad budget, instead of passing all their margins onto Google. They’ve also lowered product prices to stay competitive on the price front.

On the conference call they mentioned they planned on increasing their ad spend offline to compliment their online advertising, as online ad rates were up over 10% in the quarter, driving new customer acquisition cost up to $45 from $39 last year.

I am hoping the market is down again tomorrow and they fall further, presenting another opportunity to buy a few shares. 🙂

Their shares are off over 60% from the 52-week high of $51.60. Considering that they have no debt, are cashflow positive & over a quarter of their market cap is cash + inventory, that is quite a steep fall. I wouldn’t be surprised if a value investor pushed for a sale of the company or a PE firm bought them out, stripped the cash, loaded them up on debt, expanded them beyond medications to have a growth story which masks the cash stripping & justifies temporary losses, then listed them public again in a couple years.

During the December stock market rout eBay did not fall as much as most other tech plays, in part because a couple activist value investors were accumulating a significant stake in the company. eBay closed today up 6.13% on the suggestions by Elliot Management Corp. and Starboard Value LP to split the classifieds-ad business & StubHub from core eBay.

Late last week I traded PETS twice in a single day. Caught just about the bottom penny and then sold it for about a 1% gain. Both rather small positions, but gained about a percent on each transaction. Yesterday I bought PETS once again, but got a crappy fill on the position as the price went up about a dime a share on the market order, so when I took a nap I figured I would look again when markets open today & see the stock went from a fresh 52-week low (slightly before I bought) to actually being up a fraction of a percent on the day. I’ll likely sell it on open, as the markets are up decently in pre-market & I was up 1.47% at close & it looks like it was up another half-percent in after hours trading last night. UPDATE: sold at open today.

Pets will remain a growth market as long as birth rates across the United States remain at generational lows (& near all-time lows) as some people who would like to have children but can not afford to (economically, stress, or both) have pets instead.

I don’t see *ANY* mainstream politician with a chance at winning the next presidential election who is prioritizing the concept of family. Something like 55% of children have parents who are on means tested welfare programs now during a non-recession, and as more children are born out of wedlock to people struggling to get by economically, each broken parent acts as a walking advertisement against having kids.

Trading The Dead Cat Bounce On Analyst Downgrade

I also established a small position in Western Digital (WDC) yesterday. It quickly turned up, as a -10% day on an analyst note for a stock tied to a real business that is already quite beaten down is a bit much. I sold too early (probably in part out of frustration on the crappy fill on PETS), but still profited a bit.

If the whole market turns south WDC could fall once more, as it was at a low of $33.83 on Christmas eve & now trades at $38.06 after falling 4.92% yesterday.

We’ll likely retest those lows in the coming month.

As long as the US Federal government remains shut down Trump can blame any market turbulence on the obstructionist Democrats. In private tech executives support a hard stance on trade with China. If your profits come from IP of course it makes sense to dislike flagrant IP theft.

“I think it’s because the Chinese economy has never been more vulnerable than it is right now, and our economy has rarely been this strong,” he explained. “If we’re ever going to do anything about China, this is the perfect time. If we’re ever going to stop them from forcing our companies into dubious joint ventures that represent ridiculous technology transfers and often outright theft, this is the moment.”

China is willing to commit literal murder for leverage in trade deals – rushing already closed cases back through kangaroo courts a retrial to assign murder. In doing so, they give Trump more incentive to be belligerent in response. He gets to be the person carrying the torch fighting for human rights by crapping on them. That’s a really bad card to give him. And he could slow leak a lack of progress on the trade front on the Democrats to try to pass the buck, while further cratering confidence in Chinese markets & their economy.

It is literally what I would expect him to do. When he does that, Wall Street will be soooo pissed. They’ll tank the markets as a result too.

Other Trades

About a week ago I sold out the last of my Funko (FNKO) at a small profit. Longterm I like them, but I think they’ll have a bit of a pullback as they ran from $11 and change to over $16 a share in a couple weeks. Of course they were up to $30 not long ago too, but I wanted to exit that position for macro reasons as much as anything else.

I also bought an sold a bit of New York Times (NYT) for a small profit early in the year. I think the New York Times keeps gaining subscriber share as their weaker competitors keep getting rolled up into private equity hatchet job plays. Buying NYT is basically being long formal disinformation, political partisan hackery, and the concept of hypernormalisation.

“It isn’t real, but it conforms to my political bias” is a point that sells & many will proudly pay for, provided the first part is not advertised!

I made a small gain on AT&T as well. If yield spreads start blowing out their stock could fall on the thesis their debt carrying costs will increase.

Trade Days in a Year

I haven’t been carrying much stock or doing much trading because I did a bit of quick math and have had multiple health issues early this year (actually 4 health issues in 2 weeks is a bit of a record for terrible health for me). The math I did was thinking about there being maybe 200 or so trade days in a year. So for there to be a 6-figure income out of trading you’d have to make about $500 a day on trade days (above & beyond the cost of trading). If you could pull out a half-percent a day in trading that would mean you would need to have about $100,000 invested constantly & consistently make great trades. But there are times when the market craps the bed like it did late last year & the only winning move in such markets is often sitting on your hands. So that means maybe there are only 100 or 150 decent trading days some years.

So for that to earn 6 figures you would really need to earn closer to a grand a day on any average trade day. That would mean either needing to wring a greater return out of the market or put more capital at risk. Given QT it is hard to get excited at going long the markets right now. My risk tolerance is rather low & will remain so at least until a certain criminal fraud is caged & my faith in humanity is restored.

I am sure I could do $500 or so a day on trading if it were all I did, but being a parent who keeps getting sick & does a bunch of other things makes it a bit more challenging to have the time, focus & intensity to stay focused on it without seeing entropy eat more elsewhere.

Focused Efforts in Trading vs a Practice Account

How people will behave with fake money versus real money on the line is not necessarily the same. Sometimes people are willing to take limitless risk with fake money or money they have stolen from others. But it is not uncommon for people to have an emotional response to trades that go against them when it is savings from their own labor that is on the line.

The way to overcome those sort of negative emotional responses is to have conservative trade sizes to where you are not particularly emotional about the trades.

If you half-heartedly pay attention to the market but do not actively trade it there will be some obvious trades you should have made that you didn’t. But recognizing them at the time & seeing a few of them in a row will give you the confidence to return back to active traded – provided you are honest in what trade ideas you really liked & would actually execute on if in the mode.

One I liked – but was perhaps too lazy to act on at the time – was when Target’s stock got smashed down on a day Macy’s had the worst trade day in a decade on weak performance. I was in the line at the San Francisco Macy’s on Thanksgiving & my wife loved buying great baby clothes for 60% off there. It turns out a part of the reason their quarter stunk was they were too aggressive with early doorbuster deals and sort of had a leftoverish feel as Christmas came. Target also sold off as money was pulled out of the retail category on the narrative department stores are close to dying even though Target shared favorable numbers.

“Anybody who makes a living by selling somebody else’s widely available product, they are not going to be able to make their margin. They’re not going to be able to make a buck in this internet-driven economy,” Storch said.

I still see plenty of upside in Target providing there isn’t an imminent recession & the stock market doesn’t crater. As Walmart moves into online advertising as a marketplace player ultimately Google will be forced to acquire eBay and/or Target to remain competitive with Amazon in ecommerce. Google will ultimately need to buy a destination website with a separate brand beyond Google to win (or even remain competitive) in ecommerce. They’ll need a separate brand which is akin to what YouTube is to video.

General Work Philosophy

My philosophy has largely been one of bursts of effort based on results. Long ago I had a lot of success with SEO stuff & anything that moved in the right direction would get a lot more effort & investment. I don’t do as much web stuff as I used to, but the idea of focusing on whatever is moving in the right direction with intense focus & strong burst of effort seems a far better way to do anything than feeling you have to do it everyday.

If you work on something that isn’t producing results that ultimately impacts your mood & the quality of your work. If you internalize it enough it can impact every aspect of your life.

It is far easier to push on whatever is working until it stops responding & jump from project to project with intense, direct focus on it. That way you see results, stay positive & stay motivated.

I am mostly in cash, but am still holding a bit of Google (tech/web growth & AI advancement narrative), ExxonMobil (inflation hedge), & Apple (value play at current price). In a few months if everything goes well on the health front I might get more active with trading again.

Some of the higher volatility stocks I was trading last year like Yandex or Zillow could easily slide 10% if there is another big market pullback. If there isn’t a pullback and the trade war ends they could also quickly end up 30%, but I still expect more fireworks on the tradewar if China is literally murdering people for leverage.

Lower Entrepreneurship Risk

I suspect this year we will see a jump in entrepreneurship as the penalty for not carrying a crappy Obamacare policy is no longer enforced. This will remove $500 to $1,000 per month in junk fees from many young people who are not particularly risk adverse.

I quit my job when I was making $100 a month on the web & only had $900 in revenue in the whole first quarter of working on the web exclusively, but by the end of that year my rev run rate was above average. And I have had many good years in spite of a number of major setbacks including dealing with many major algorithm updates, major health issues, and a few other treats I’ll mention in due time.

The web is certainly far more saturated with competition today than it was when I started, but it is also far easier to find great information in just about any format you’d like: blogs, podcasts, forums, newsletters, Twitter, etc.