I think it was the venerable Jim Grant who I remembered hearing emphasize that markets are reciprocals. Risk is what you take, price is what you pay & value is what you get.

Quite often the explanation after the fact is getting cause and effect backward.

Bonds strengthen with volatility, leading to market sell off.

Um maybe the market falling caused the spike in volatility & rush into bonds?

The flattening then inverted yield curves across many countries do not happen in isolation of cause.

The Yuan has slid to offset tariffs, though perhaps not enough to put them on a currency manipulator list. Other regional Asian currencies have been weak as well. Kyle Bass put out a paper on the quiet panic in HK, noting how he believes the HKMA has spent north of 80% of their usable reserves defending their peg to the US dollar & the Singapore Dollar has been slipping too.

Turkey is doing Turkey.

I remember drinking there back when I was in the Navy & we pulled into port on my 21st birthday. They had a lot of zeros on their currency, as they will soon have again.

Huawei maintains their R&D budget is being spent on innovation rather than theft. They say we need them more than they need us & they are fine without us.

Yet they claim their blockage from the US market is unconstitutional.

If tariffs were costing US households $831 each & Huawei technology was legitimately superior I am skeptical we’d go through with cutting them off. Their wholesale theft of Cisco IP including the typos in user manuals would indicate their “tech” is more recycled than cutting edge.

Rather their theft-based economic growth miracle is coming to an end. It is smart for the US to do unto China as China would do unto others. If they block your legitimate enterprises based on “security” to drive subsidies for home grown (cloned?) competition, then block their tech exports based on “security”

If things are unbalanced & such lack of balance is hollowing out your economy you need to launch economic grenades at the other side so they eat a bit of their own home cooking.

Not to mix metaphors, but… nothing is more unpalatable than home cooking when the chef knows the cut rate foods that made the ingredient list to create the poisoned stew.

Other countries like Japan are implementing foreign ownership limitations in vital economic areas like IT & telecom.

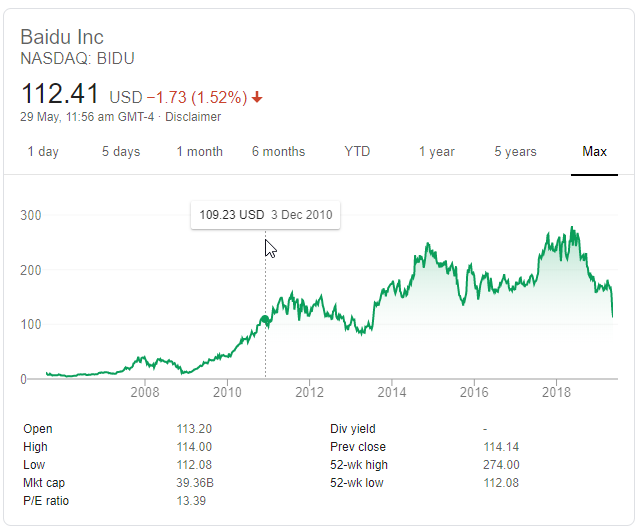

Baidu is priced like a heavy industrial commodity tied to a cyclical company that has been through a couple bankruptcies in the past 20 years. Baidu’s share price is around where it was at the end of 2010. Skepticism is high & even a $1 billion buyback announcement had no real impact on the decline, as that is only about 5% of their investible capital & they might further dilute the company by listing it in China.

Each day their stock looks cheaper than the past. But how low might they go if the fleeing foreign capital is followed up by a bit more selling to drive the price down in order to repatriate the company as a whole?

Think of how much stimulus China has done in the past decade (via the rule of 72 & an 8% growth rate they’ve more than doubled) & yet such a core company tied to the rapid growth of the web – sitting in a monopoly position – has went nowhere in terms of market cap.

Net buybacks have had a bigger impact than most would believe.

net buybacks—the number of shares that companies repurchased across the entire stock market, less the number of new shares issued—explain the bulk of the intermediate- and longer-term differences in stock-market returns around the world. … China’s real GDP, in U.S. dollars, grew at an 8.0% annualized rate over the 10 years through year-end 2018, versus a 2.1% annualized rate for U.S. GDP. And yet U.S. equities’ annualized return over this decade was more than double that of China’s. … net buybacks explain 80% of the difference in countries’ returns between 1997 and 2017. … The researchers calculated that the issuance of new shares in the Chinese market—largely as state-owned enterprises went private—had a “massive dilution effect” of nearly 24% a year between 1997 and 2017. Little wonder, therefore, that the country’s equities struggled over this period, despite its economy’s incredibly fast growth.”

Alibaba – the great company that it is – is considering a dual listing in HK. Those share sales would be in spite of recent weakness & would be the opposite of a buyback. Why rush to buy any of it with that risk in place & momentum clearly to the downside: “China’s central bank has warned in a report that uncertainties brought by trade frictions between China and the United States could have an adverse impact on the global economy.”

As far as the broader stock market goes we are back in December in terms of momentum. Jawboning isn’t really driving the markets: “the short-squeeze in yuan lasted around an hour, before sellers returned… Erasing all Guo’s hard jawboning work.”

For now we’ll sit on the sidelines as China sticks to a managed decline:

Their strategy is perfectly clear, therefore also the implications. Managed decline. … But in order to manage just that minimal growth in currency, the dollar squeeze on the asset side means something has to give. The only thing left, China’s big monetary fudge factor or plugline, is bank reserves. Therefore, in order for currency to stay positive bank reserves have now to contract by around 8-10% every month.

The Federal Reserve can’t eat the risk of stoking further inflation until there is some other fire they are fighting:

The leader of the free world has a super hero name for himself and it’s “Tariff Man“, a state of affairs you’d think would be conducive to inflation. As it happens, Tariff Man has a penchant for pro-cyclical fiscal policy that borders on the fanatical. Again, that should be conducive to inflation, as piling fiscal stimulus atop a late-cycle dynamic when unemployment is parked at a five-decade nadir is tempting fate, assuming the Phillips curve is “just sleeping” (and not “gone to meet its maker”, like the Norwegian blue). And “Tariff Man” is also engaged in an around-the-clock effort to commandeer monetary policy, which he’d like to be pro-cyclical too. One more time: That should be conducive to inflation.

Our solution to every bump in the road is more intervention versus more capitalism:

“The economic engine we have in place today has for decades produced virtually no increase in wealth for the majority of earners. According to information pulled from the Federal Reserve, the median net worth of the bottom three quintiles of families declined in inflation-adjusted dollars from 1998 until 2013, tumbling by 20 percent or more. This decrease has hit working-class families the hardest; their real net worth has been halved over this time. … I’d argue that we don’t really have all that much capitalism anymore. Individuals simply do not have equal, competitive rights to own the means of production. Corporations, which have replaced both the feudal empires of the 1600s and the trusts of the early 1900s, are the contemporary preferred owners of capital goods to be extended privileged rights by central governments. … With Blackstone able to offset the cost of its 400 lawyers against $5 trillion of assets, how can small banks or asset managers compete? The answer is they can’t, so they get acquired (or go out of business). … researchers at Harvard Business School have shown that favorable merger reviews are more likely for firms that make large political donations to the politicians who sit on the two committees that oversee the FTC and the DOJ. … From 1950 to 1980 or so, prices on average goods were marked up roughly 18 percent above marginal cost; this level was largely stable during the entire period. However, beginning in the 1980s, prices began to rise, rocketing to 67 percent above cost today. When you are an oligopoly and customers have no real choice among the top three to five providers, you don’t need to openly collude. Just all raise your prices together, and customers are stuck. … it’s critical for the government to normalize the legal rights of individuals to, at the very least, give them equal status with the current preferred neofeudal empire, the corporation.”

The belief in the Fed put is a mistake because they’ll have to wait for the market to crash before they can use the market crashing as pretext to intervene further.

Once they indicate they’ll buy ETFs it is off to the races.